Benjamin Franklin says ‘An Investment In Knowledge Pays The Best Interest‘ that means invest smartly with strategic approach to grow your wealth by making informed, calculated, and disciplined investment decisions rather than just putting money into assets that generates returns. The 10 Rules of Smart Investing tells best practices for building wealth and taking care of your future self.

Smart investment focuses on maximizing returns while minimizing risks through diversification, long-term planning, and data-driven choices.

Smart Investing = Strategy + Discipline + Patience

1. Start Now

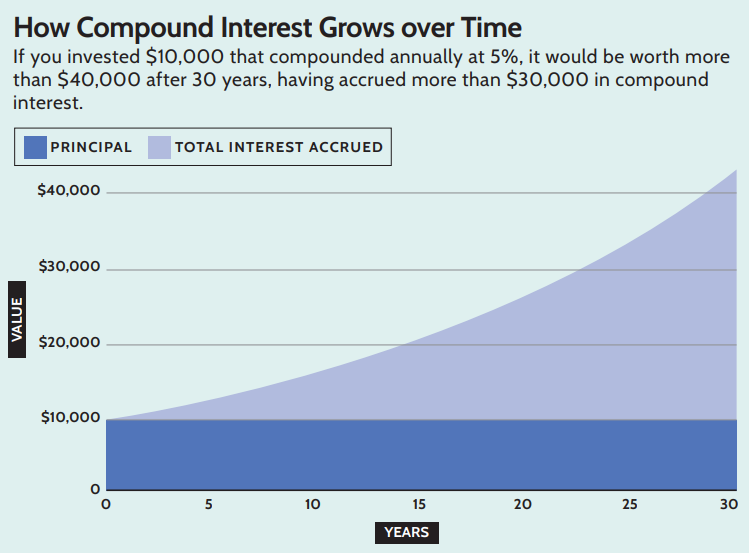

The first key to investing is starting as soon as you can, putting aside money now with the goal of achieving long-term wealth, so that your future self will be in a stronger financial position. Money you invest now compounds over time, earning interest that is then reinvested, allowing the principal investment to grow. The longer you leave your money to compound, the more it will grow, generating even larger interest payments.

“Not investing is worse than being invested during challenging markets.” – Preston Cherry the founder and President of Concurrent Financial Planning.

When you have time on your side, you have the ability to allow your investments to compound over the long term and create a more productive, prosperous portfolio.

Investing as soon as possible, and staying invested over the long run, tends to be more lucrative than waiting and trying to invest at exactly the right time, based on when the market is up or down.

2. Economy & Market

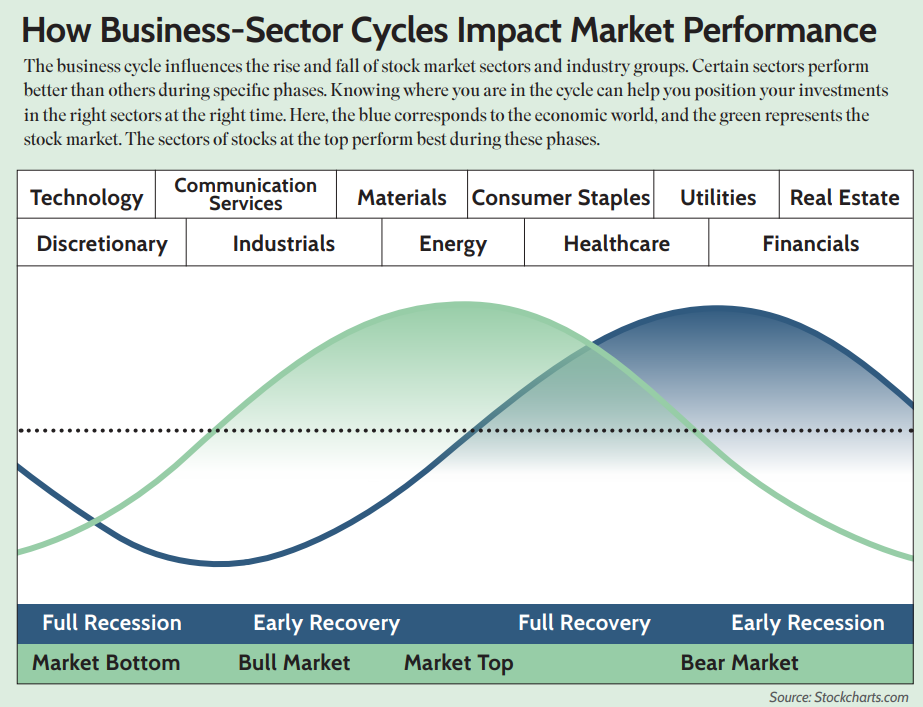

When the economy is growing along with expansion of business activities, leads to stock market gains and improving returns for investors. When the stock market slumps, that results in losses for investors and a decline in consumer confidence, leading people to spend less, which can cause a downturn in the economy.

A financial market is the place where people buy and sell investments, such as securities, currencies, and bonds. While the two are different, they influence each other

It’s going to go up and it’s going to go down, and sometimes the down is going to scare the heck out of you. The biggest thing you cannot do is panic and take your money out. Because as history shows us, the market always comes back. And when it comes back, it usually goes to new heights.

The stock market is a leading indicator of the sentiment of the country’s economy. It’s a reflection of how people are feeling, and money, unfortunately, is emotional. So we have to understand that there are going to be current, short-term fluctuations.

3. Time is Money

The right investing approach will vary for each person depending on a range of factors, including their age, stage of life, and financial goals

Those who are investing when they’re young and at the beginning of their career should take a different approach than those who are older and approaching retirement. Younger investors can tolerate more risk than older investors. Typically, young people can afford to take more risks while investing because retirement is still decades away for them. Meanwhile, older people should pursue more stable stocks and bonds as part of a balanced portfolio.

If your goal is to buy a house, are you aiming to do that in five years or 15? If you’re saving for retirement, are you aiming to retire in 20 years or 40? Investors should use those goals and timelines to determine their individual investing strategy.

“With a good perspective on history, we can have a better understanding of the past and present, and thus a clear vision of the future.” — Carlos Slim Helu

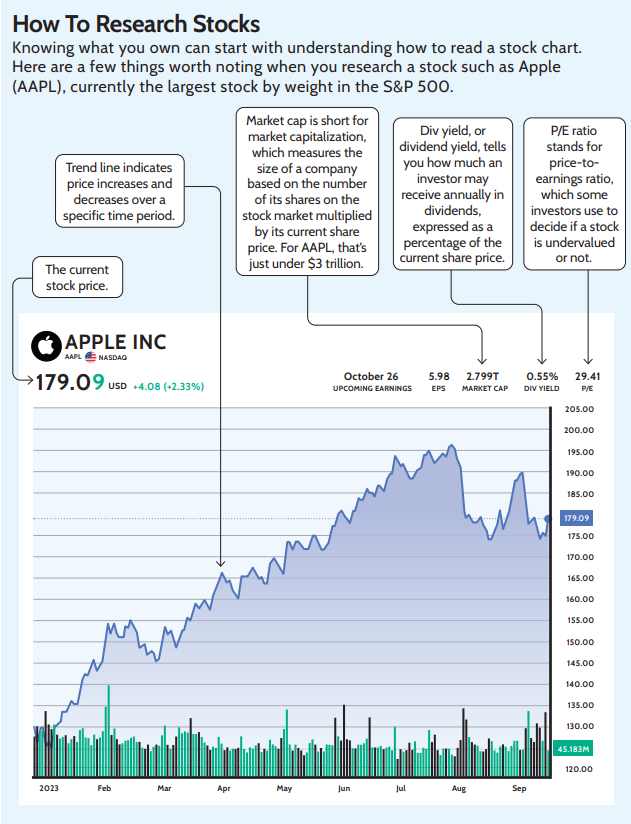

When deciding whether to buy, sell, or hold a stock or fund, it’s important to start by doing research. If a company is sustainably growing revenue year-over-year, and if the company’s future earnings are predicted to grow, it could be a good time to buy that stock. It’s better to focus on details and data points that suggest long-term growth and stability rather than a short-term bump

4. Target Balanced Investment

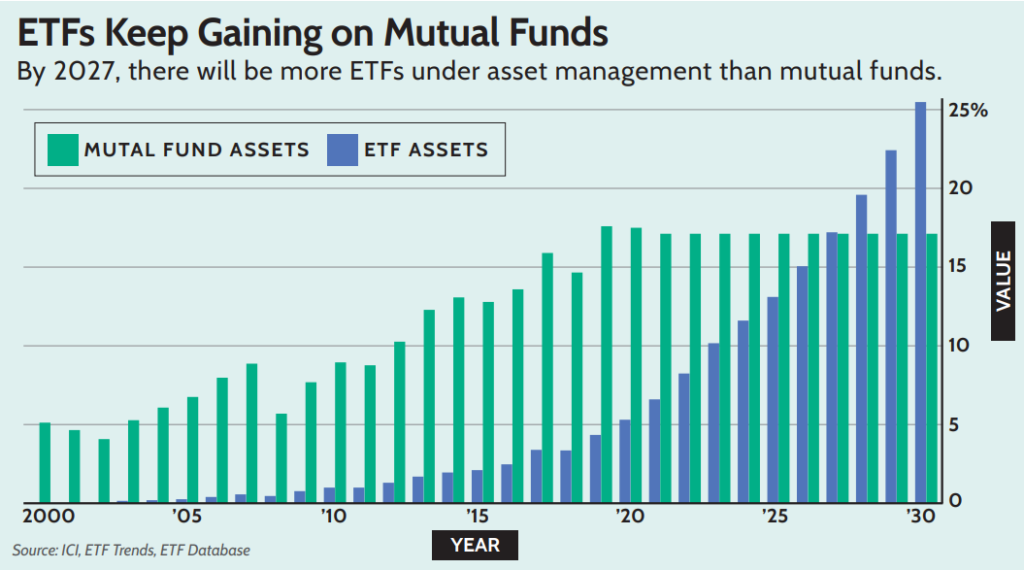

A portfolio is the mix of all of a person’s investments. A balanced portfolio includes investments in a diverse variety of assets—including stocks, bonds, gold, real estates, mutual funds, or exchange traded funds (ETFs)—to reduce volatility. The process of investing in those different asset classes is known as diversification. Reduces risk if one asset class underperforms.

Don’t dump all of your money into one investment. Diversify your portfolio with different types of assets so that when one company is not performing well, all of your portfolio is not damaged because of that

Experts recommend that investors regularly review their portfolio and make changes, or “rebalance,” when necessary maybe once a year, to make sure their portfolio is still allocated in the way they would like.

For example, if an investor built a portfolio with 60% stocks and 40% bonds, but over time the portfolio shifted to a combination of 70% stocks and 30% bonds due to market performance, the investor could review and readjust their portfolio back to the original allocation in order to meet their financial goal. But the conventional wisdom is that 60% stocks and 40% bonds is a really safe, easy way to think about it.

Experts suggests starting from that combination of stocks and bonds and then potentially moving smaller percentages into other investments, such as cash, gold, real estate funds, or global stocks. Investing a small portion of your portfolio in global stocks markets in US, Singapore, or South Korea, can help support balance.

However you choose to divide your investments, it’s most important to ensure that you’re not investing all your money in one place.

5. Buy What You Know

Buy what you know. Don’t invest in things that you can’t explain to somebody so they understand. It’s important to understand how your portfolio is allocated and what purpose each asset is serving.

When considering which stocks to buy or sell, there are several data points that are helpful to understand. Look at the market’s general direction, such as the moving average of the Standard & Poor Index

Goal-Oriented Investing: Define your financial goals (e.g., retirement, buying a house, child’s education).

Align your investments with your time horizon (short-term, medium-term, long-term).

Knowing what you’re invested in is also critical if you’re interested in putting your money toward certain issues or causes, such as environmental or social issues.

Key Research points before invest in stocks:

- Balance Sheet: The balance sheet plays a crucial role in stock research, providing a snapshot of a company’s financial position at a specific time. Investors analyse the balance sheet to assess the company’s financial health, including its assets, liabilities, and equity.

- Income Statement: The income statement is also called the profit and loss statement. It is critical for stock research. It gives insights into a company’s financial performance in a specific period. Investors analyses the income statement to assess the company’s revenue, expenses, profit, and efficiency.

- Cash Flow Statement: The cash flow statement is a vital financial document. It shows a company’s liquidity, operations, and health. In stock research, the cash flow statement has many vital roles. It assesses liquidity, operating performance, capital expenditure performance, and financing activities.

- Online Stock Research Websites

- Understand the Numbers: Analyze financial ratios and metrics. They show the company’s performance. Key ratios include:

- P/E Ratio: The P/E Ratio measures a company’s current stock price relative to its earnings per share. It is also called the price-to-earnings ratio. It can be forward-looking, using estimated earnings, or backwards-looking, based on past earnings.

- PEG Ratio: The PEG Ratio compares a company’s P/E ratio to its yearly earnings per share growth. It shows its valuation relative to its growth prospects.

- P/B Ratio: The P/B Ratio compares a stock’s price to the company’s book value. Book value is what the company could get by selling all assets.

- Learn About The Company

6. Control Your Animal Spirit

“People set goals that are too high, and they take on imprudent risks as a result—risks that, on average, don’t pay off.”

There are strategies people can use to balance their emotions and make optimal decisions. Before deciding to sell stocks, for example, experts suggest sleeping on it and reevaluating the decision in a day or two. Investors should also avoid checking their portfolios too frequently. Instead, make a plan to check in quarterly or meet with a financial advisor semi-annually. Investors should also avoid making decisions based solely on intuition.

The greed can lead people to want more than their fair share. Neither excessive fear nor excessive greed is good.

7. Play Safe Than Sorry

Exercise caution when making big investment decisions. Do research and consider your options carefully before making any rash decisions with your money.

Experts says It’s “dangerous” to borrow money to invest, noting that positive returns are not guaranteed, and investing borrowed money exacerbates the potential for negative consequences if an investment doesn’t perform well.

Similarly, investors should think twice before tapping their retirement accounts early—in part because they will be subject to penalties if they do so, though there are some exceptions. Money withdrawn from an individual retirement account or withdrawal from PF before continuous service of 5 years become taxable.

The cautionary tale for investors about the prevalence of low-quality financial advice floating around on the internet. The lesson: Make sure you’re taking advice from reliable sources, and don’t do something just to follow a friend, family member, or influencer. “Don’t invest in an asset just because your best friend is doing it”

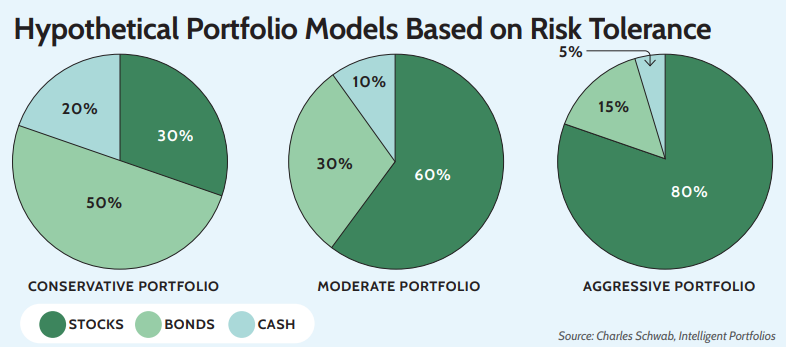

8. Risks Managements

Balances risk and reward based on risk tolerance (Conservative, Moderate, Aggressive) and market conditions.

Invest accordingly:

- Low risk → Fixed Deposits, Debt Mutual Funds, PPF

- Medium risk → Index Funds, Large-cap Stocks, Gold.

- High risk → Small/Mid-cap Stocks, Crypto, Startups

9. Be A Tax Efficient Investor

Being tax-efficient means paying the least amount of taxes required by law. It’s important for investors to be mindful of tax rates, which differ depending on the asset and the type of income

Choose low-cost investment options (e.g., index funds vs. high-fee mutual funds). Use tax-saving investments like PPF, ELSS Mutual Funds, NPS.

10. Automate And Maintain Consistency

Automating your investments–setting up regular contributions from your paycheck or bank account is a great way to form an investing habit and stay consistent. It also ensures that you won’t be tempted to use that money for something that’s not a necessity, or make an excuse about not wanting to invest that month.

Use Systematic Investment Plans (SIPs) for disciplined investing. Set up auto-deposits to avoid emotional decision-making.

Look at the monthly or quarterly statement from your brokerage firm, and consider rebalancing your portfolio maybe once per year. But also resist the urge to constantly check your portfolio to see how your investments are performing.

Smart Investing Summary

Investing is just putting money in assets. Smart investing is doing it strategically, patiently, and with risk awareness to build long-term wealth.

Smart Investing is an essential in building the future you want for yourself, and the best thing you can do is start now. Take advantage of the “magic of compounding” by investing early and allowing your portfolio to grow over the long term. Build a balanced portfolio that will help you weather market fluctuations. Make automated investment contributions, but stay informed about what you’re investing in and when you might need to make adjustments. And manage the level of risk you take on by doing research through reputable sources and building a diversified portfolio with a combination of assets that feels comfortable for you.

Don’t expect to see instant results or to make perfect investing decisions, but keep your long-term goals in mind.